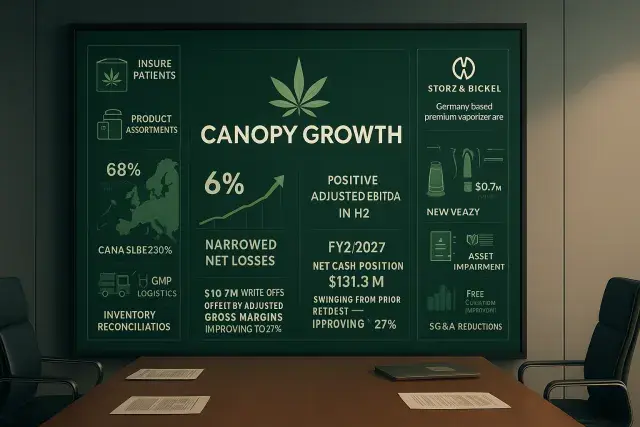

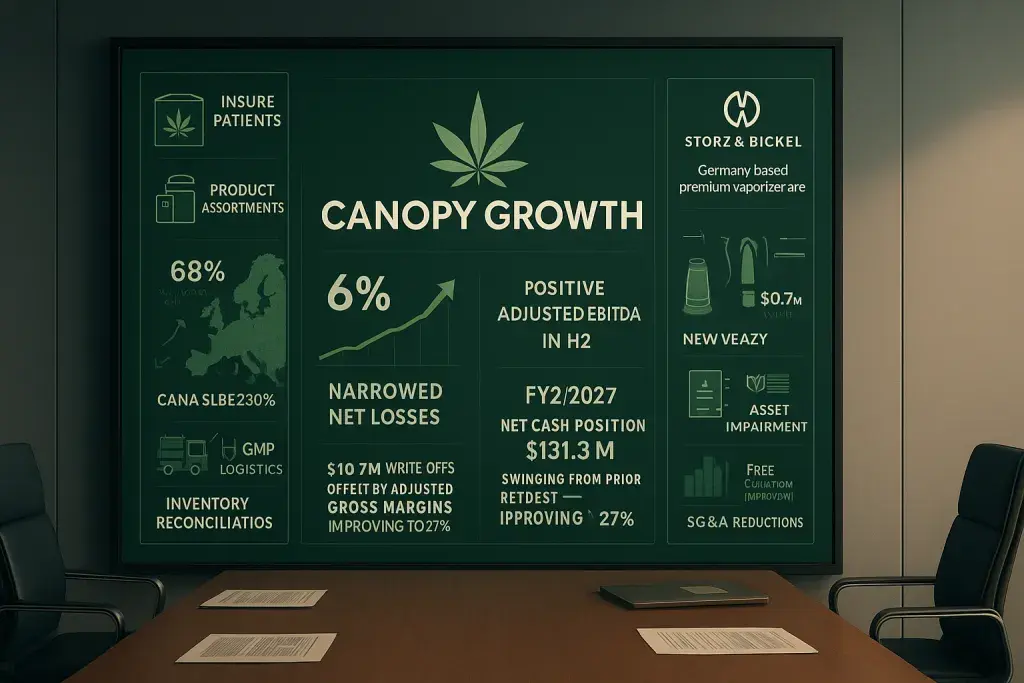

Canopy Growth closed its fiscal year ended March 31, 2026 with consolidated net revenue of $284.6 million Canadian - a 6% increase over FY2025 - and a narrowed net loss from continuing operations, but the company has not yet reached positive adjusted EBITDA. The improvement is real; the finish line is not here yet. The company is now explicitly targeting positive adjusted EBITDA during fiscal 2027, with the bulk of year-over-year improvement expected in the second half of that year as MTL Cannabis integration costs wind down.

For operators and suppliers watching cannabis market consolidation, the MTL Cannabis acquisition is the structural move that defines Canopy's FY2026 story. MTL added cultivation capacity and supply, but it also triggered $10.7 million in inventory write-offs in Q4 alone - a consequence of reconciling combined inventory levels post-close that pushed consolidated gross margin down to 12% for the quarter. That kind of one-time inventory pressure is a familiar cost in cannabis M&A, and it is worth understanding the mechanics: when two licensed producers merge, overlapping SKUs, shelf-life constraints, and compliance-driven batch tracking requirements can force write-downs that look ugly on a single quarter but reflect cleanup rather than ongoing operational failure. The same discipline applies at the retail end of the supply chain - operators running a cannabis pos system maine or any other regulated market know that inventory reconciliation isn't optional; seed-to-sale tracking requirements make accurate batch-level accounting a compliance obligation, not just a financial preference. Excluding the MTL-related inventory step-up and write-offs, Canopy's adjusted gross margin for Q4 FY2026 was 27%, compared to 19% in the same quarter the prior year - a meaningfully different picture.

Canada Medical Cannabis Drives the Growth Narrative

The clearest bright spot in FY2026 was Canada medical cannabis. Revenue reached $25.3 million in Q4 FY2026, up 27% year-over-year, driven by insured patient growth and a broader product assortment. For the full year, Canada medical cannabis revenue rose 18%. Canopy now describes itself as the leading medical cannabis provider in Canada by revenue - a position it is explicitly planning to extend into European markets.

Europe is the strategic bet here. International markets cannabis revenue fell 7% for the full year due to supply chain disruptions earlier in FY2026, but Q4 showed a sharp recovery - 68% growth versus Q4 FY2025 as those supply constraints were addressed. Supply chain execution in regulated cannabis export markets is operationally demanding: EU-GMP certification, country-specific import approvals, and batch documentation requirements create lead times and compliance friction that domestic operators rarely encounter. Canopy's ability to recover Q4 international revenue after stumbling mid-year suggests the underlying logistics infrastructure is functioning, even if it proved brittle under pressure.

Storz & Bickel Faces a Tougher Market

Not every segment improved. Storz & Bickel - Canopy's Germany-based premium vaporizer brand - posted $70.7 million in revenue for FY2026, down 14% from FY2025. Gross margin contracted from 37% to 33% for the year, with tariffs on U.S. imports and geographic mix shifts compounding the impact of weaker consumer demand. The company recorded $67.1 million in asset impairment and restructuring charges in FY2026, primarily tied to Storz & Bickel goodwill and brand impairments alongside employee restructuring costs. That is a significant non-cash charge, and it reflects a realistic reassessment of what was paid versus what the business is delivering in the current consumer environment.

The new VEAZY vaporizer, launched in September 2025, is positioned in the more accessible price tier - a deliberate move toward affordability and portability. Whether that repositioning gains traction will be visible in FY2027 results. The thing is, consumer-facing hardware in cannabis accessories competes against a wide range of price points, and brand premium only holds if distribution and product quality consistently back it up.

Balance Sheet Repair Changes the Strategic Equation

The most consequential number in Canopy's FY2026 results may not be revenue at all. The company ended the fiscal year with a net cash position of $131.3 million Canadian, compared to net debt of $172.6 million at the end of FY2025 - a swing of roughly $304 million. Free cash outflow also improved sharply, from $176.6 million in FY2025 to $69.1 million in FY2026. For a cannabis company that has spent years burning cash while restructuring, that balance sheet shift materially reduces refinancing risk and gives management the flexibility to execute without a creditor deadline driving decisions.

SG&A fell 6% year-over-year in FY2026, reflecting headcount reductions and lower third-party costs across insurance, professional fees, and IT. These are real operating savings, not accounting adjustments. The adjusted EBITDA loss narrowed to $20.2 million for FY2026 from $23.5 million in FY2025 - modest progress, but directionally consistent with the FY2027 profitability target. Canada adult-use cannabis, meanwhile, posted 20% full-year revenue growth, supported by infused pre-roll joints and new vaporizer formats - categories that have shown consistent demand across several regulated markets. The adult-use side of the business is not the company's primary focus in its forward strategy, but it is not a drag either.